What’s Wrong With My Money?

ARC101 – What’s Wrong With My Money?

Welcome to Part 1 of the CryptoCoinMindSet Educational Arc.

Before we can talk about what cryptocurrency is, how to buy it, or how to secure it… we have to answer the most important question of all… Why?

Why does any of this matter?

I’m going to guess you’ve felt it once or twice before… probably the last time you went to the pump… or the grocery store…

You know what I’m talking about… that quiet sense that your money doesn’t go as far as it used to…

I’m here to tell you that its not your imagination…

That IS the design of the system… the design of the machine we’re living in…

What I’m going to outline for you today isn’t going to be a history lesson… it’s going to be a story… and an outline… of the single greatest transfer of wealth in history…

A transfer that’s happening in slow motion… right in front of our eyes… and it’s been running on the same playbook throughout history…

Today I’m going to expose this debasement… to open your eyes… to expose the lies… while you still have time to escape…

Part 1: The Hidden Tax – Deconstructing Inflation

The government and the media tell you that this “inflation” thing is a normal part of a healthy economy…

They tell you that it’s “supposed to increase annually at a rate of about 2-3%.

But what if that number is a lie?

What if inflation isn’t a natural phenomenon… but a hidden tax?

What is it was actually a deliberate… silent theft… that erodes your savings, and your purchasing power… and it transfers your wealth to someone else.

What Inflation Really Is

The official story is, that inflation is “a general increase in prices and a fall in the purchasing value of money.”

This definition is designed to confuse you… it makes it sound like prices are just going up on their own… as if it’s a natural force of nature.

But here’s the truth… prices don’t just go up…

What you have been led to believe is inflation, is actually the value of the thing you’re using to buy goods & service (USD)… your currency… going down.

So, what is inflation… really?

Inflation is the devaluation of currency… plain & simple!

Governments and central banks increase the supply of money and credit…

We’ve seen this playbook play out multiple times throughout history, with one of the most recent and notable examples being the massive money printing that happened during the COVID-19 pandemic.

Let me give you an example of how this works…

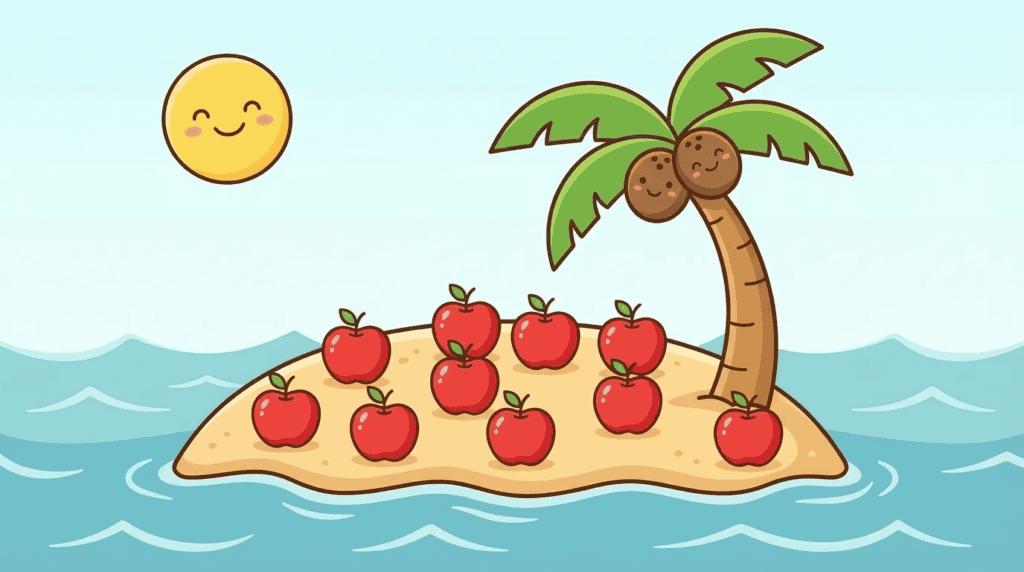

Let’s say you’re on an island… and on that island there are 10 apples and 10 dollars… so the cost of each apple will be $1.

But if a helicopter flies over the island… and instead of recuing you… it drops another $10 onto the island.

So, you now have $20 dollars chasing the same 10 apples.

The price of an apple will now rise to $2.

The apples didn’t become more valuable… the dollars became less valuable.

So, to recap… inflation isn’t prices going up… it’s the value of your money going down.

The 2% Lie

This brings me back to something I mentioned earlier… the official inflation target of 2-3%.

This is a target created by the central banks… like The Fed. They claim is that this increase is actually healthy for the economy… but that is a lie.

But The Fed is smart… they didn’t just choose this rate arbitrarily…

NO, NO… this is a carefully chosen rate of theft.

Why?

Because this target… it’s roughly in line with the average amount of new gold that gets mined, and enters the market every year.

Right now you might be thinking; what does gold have to do with inflation?

Believe me… I get it… it took me a while to see it…

But as we’ll discuss when I lay out the principles of sound money… gold has been the best money the world has seen throughout history… it has been used as a medium of exchange for millenia…

So, by setting their target to match the natural rate of increase for a real… hard asset… they create a illusion of stability.

It makes their fiat currency appear to hold its value relative to gold… when in reality… both are rising in nominal price to hide the fact that your paper currency is constantly being devalued.

But that’s not the only slight of hand going on…

How They Fool You: The CPI Con

In order to come up with the “rate of inflation,” they have to measure it.

So how do they do that?

Well, the most common number you hear them use is something called the Consumer Price Index (CPI).

The Bureau of Labor Statistics sends out “secret shoppers” to track the prices of a “basket of goods.”

Supposedly, this basket of goods is what a typical household buys.

The problem is… this basket is a manipulated fantasy.

To keep the official number low… they engage in something called “substitution.”

What does that mean?

Basically, if the price of steak gets too high… they remove it from the basket, and substitute cheaper hamburger.

Frankly, they assume you will happily make the same downgrade… so your cost of living hasn’t really gone up.

But when they substitute a lower-quality item within the same category… it’s to just game the numbers… it’s meant to be a complete deception.

Now, I want to be fair…

Obviously some substitutions are necessary… I’m going to guess that people aren’t buying VCRs & rotary phone too much these days…

But, when they downgrade an item… like steak to hamburger… I think you get my point…

But the manipulation doesn’t stop there…

There numbers also use something called “hedonic adjustment.”

Let me see if I can break this concept down is simple terms for you…

Basically, this is where they claim that even if the price of an item goes up… you’re not worse off, because the quality has improved.

For example, let’s say a new smartphone costs $1,200… which is $200 more than last year’s model.

But if they decide the new camera in this new model is “worth” $250… they will actually record the price of that phone as having gone down by $50 in their inflation calculation.

They use this subjective quality adjustment to magically lower the reported inflation on everything from computers to cars… even as your out-of-pocket cost rises.

One final point on these calculation numbers…

They don’t include the cost of housing or energy.

Yeah… you read that right…

The 2 biggest line items in the budget of most households… housing & energy… aren’t even factored in.

Why?

I mean… make it make sense…

I’ll try…

They say that these items are excluded because their prices are “too volatile”… and admitting the true cost of shelter and fuel would obviously reveal a much higher inflation rate.

I guess the good news is… they do actually calculate these costs… though the “how”…

So why do I sound a bit disgusted?

Because when they calculate housing costs… they don’t use the actual price of a home… they use something called “Owners’ Equivalent Rent.”

And what is Owners’ Equivalent Rent?

In a nutshell, it’s a survey-based guess… a guess of what homeowners think they could rent their house for.

A guess… a guess only certain people can even respond to… have you ever gotten one of these surveys?

I haven’t.

And bonus… this number often lags behind reality… and significantly understates the true cost of housing.

The Real Numbers

After all of this, you’d think I’d be done…

But I’m not…

The final thing you need to understand about these inflation numbers is… their not real.

The official headline CPI is a heavily manipulated political tool… designed to keep cost-of-living adjustments for things like social security, and union contracts, as low as possible.

But organizations like ShadowStats… which use the government’s own calculation methodology from 1980… show that real inflation has been running much higher for decades… often double or even triple the official rate.

They are lying to you about the rate of inflation to hide the fact that they are actively stealing your wealth.

Inflation is a brutal… regressive tax… that punishes savers… rewards debtors… and widens the gap between the rich and the poor.

Part 2: The Unfair Game – The Cantillon Effect

Now that we understand what inflation is… we need to understand how it’s distributed.

Because believe me when I tell you… it’s not distributed evenly.

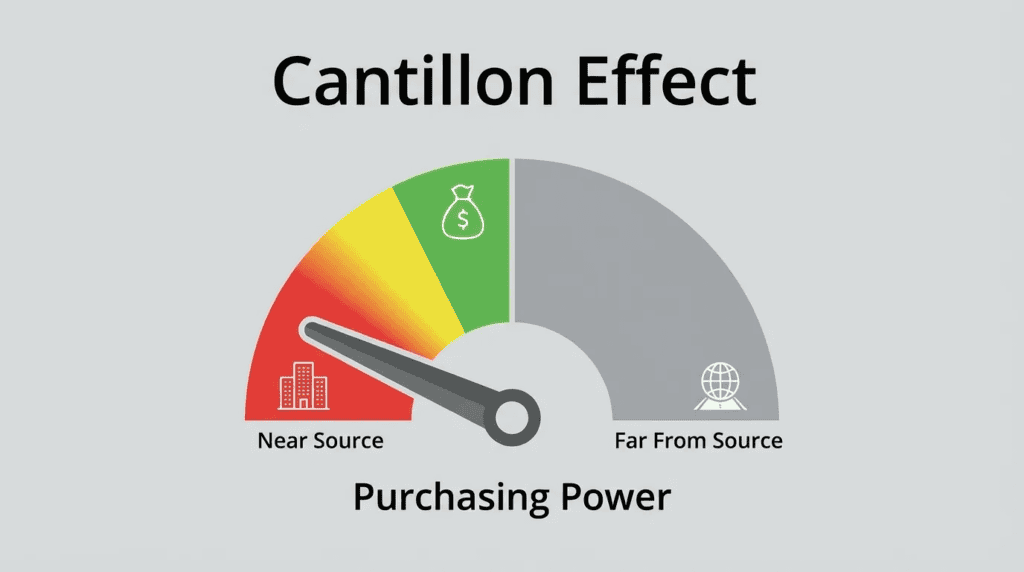

This silent theft has a name: the Cantillon Effect.

What is the Cantillon Effect?

Cantillon Effect… it almost sound a bit conspiratorial, doesn’t it?

Well is nothing quite that grandious… it’s basically a fundamental principle of how new money distorts an economy.

The name, Cantillon Effect, comes from an 18th-century economist named Richard Cantillon.

He observed that when new gold entered the system… the first to touch it… always came out ahead.

How It Works Today

So, here’s how this effect works within “the machine” today.

When the government needs money… it sells bonds.

To buy those bonds, The Fed creates new money… new debt… out of thin air I might add…

This IS the first gear in the machine turning.

That brand new money goes to the government first.

They spend it on massive contracts… salaries… and various social programs.

The first recipients of this new money… like defense contractors and big banks… well, they get this new money at its full, original purchasing power.

They are the first cog in the system to benefit from its creation.

But here’s the part that affects you…

This new money isn’t spent to create more factories or jobs… these new dollars just chase the same amount of goods that already exist… this IS the very definition of inflation.

Think of it like a poker game where one player gets to add new chips whenever they want… the more chips they add.. the more it costs the other players to remain in that hand.

So this new money gets spent and invested.

This forces the prices of the assets up.

And here’s how that affects you and me…

By the time this new money trickles down to you as a wage increase, or a small business loan… the value of your dollar has already been eaten away by this hidden tax.

You and I get this new money last… so we’re paying prices that were driven up by the people who got it first.

Make no mistake… this isn’t a side effect of the machine… it’s the machine’s primary function.

It IS the mechanism that the machine uses to transfer our wealth… our economic energy… to the elite.

This IS why the stock market keeps hitting all-time highs, while your paycheck buys less.

This IS the Cantillon Effect in action… the rich get richer, and you and I get the bill.

Part 3: The Crushing Burden – The Sovereign Debt Spiral

So, we have a hidden tax (inflation)… and an unfair distribution mechanism (Cantillon Effect)…

but the final piece to the puzzle is the motive.

Why would the government do this?

Basically, our government has a spending problem…

In short… the answer is debt.

What is the Sovereign Debt Spiral?

So, how exactly does a government borrow money?

The government doesn’t “borrow” money like you or I do.

It doesn’t go to a bank… ask for a loan… and promise to pay it back with interest…

When a government needs money, it sells bonds.

A bond is basically a government IOU.

Once it creates these IOUs, it sells them to the Federal Reserve.

And what does the Federal Reserve do?

If you don’t already know… The Fed doesn’t have any money sitting in a vault… its ‘checkbook balance’ is literally ZERO.

So, what does the FED do… they create new money… out of thin air… to buy those bonds.

That’s not borrowing… that’s printing.

And here’s where it really starts to get wild…

Every single dollar the government needs to pay that interest on this spending… must also be borrowed into existence.

That’s right… the interest payments… they’re not paid with tax revenue… they’re paid with more debt.

So, when you hear all this talk about the “debt ceiling”… and you hear politicians screaming about “fiscal responsibility”… what they’re really talking about is how much more they’re allowed to borrow… how much money they’re allowed to rob from future generations… just to pay the interest on what they’ve already borrowed.

Our current financial system is a Ponzi scheme… a Ponzi scheme that’s been stamped with a government seal of approval.

The Inescapable Cycle

As of today… the U.S. national debt is quickly approaching $40 TRILLION… and is growing to the tune of approximately $1 TRILLION every 90 days.

To pay the interest on that new borrowed money… they need to borrow more…. and to pay the interest on that… they borrow even more.

This is the sovereign debt spiral.

The more the government borrows… the more it has to pay in interest... the more it pays in interest… the more it has to borrow… And the more it borrows, the more it has to print… which drives up inflation… which drives up interest rates… which drives up the debt…

And the cycle continues… again… and again…

This isn’t a side effect… or an error… IT IS the design of our current system.

The machine is built to never be paid off the debt… it’s built to keep you paying… in the form of higher prices… lower wages… and a weaker dollar.

This is the silent theft… it’s happening every single day… and it’s not going to stop… it can’t… or the entire system just falls apart.

Realize That The System IS the Problem

So, if you’re to believe the government… the official story is that this is all a mysterious… sometimes difficult-to-control force… that’s a necessary byproduct of a growing economy.

They tell you a little bit of inflation is good… that it’s a “greasing of the wheels” of commerce… that’s a lie.

Inflation isn’t a mysterious force… it’s a policy.

The Cantillon Effect isn’t an accident… it’s the operating manual.

The debt spiral isn’t a mistake… it’s a feature.

It’s a predictable… deliberate… and silent tax on your wealth.

These are the 3 pillars of a single… interconnected system… that’s designed to transfer wealth to the top.

Inflation is the mechanism… Cantillon is the unfair distribution… and Debt is the motive.

This is not a series of unfortunate accidents or economic miscalculations.

It IS a predictable, repeating pattern driven by a single… unchanging motive… a government’s insatiable need to fund its operations without the political consequences of direct taxation.

This entire process is a direct assault on your future.

It targets your savings… especially your retirement savings.

The person who works for 40 years… diligently putting money into a 401(k) or a savings account… is being systematically robbed.

The $100,000 they think they have, will only have the buying power of $50,000 by the time they retire.

It’s a promise that is systematically broken by the very system that told them to save in the first place.

But the good news is, for the first time in history… you have a choice.

You can opt out.

Now that you see the machine for what it is… you can’t unsee it.

It’s time to make your move.

Your journey into financial sovereignty starts with understanding the solution.

Your next step is here: The 7 Pillars of Sound Money

Disclaimer

The information provided here is for INFORMATIONAL & EDUCATIONAL PURPOSES ONLY!

View our complete disclaimer on our Disclaimer Page