Cryptocurrency: What Are Stablecoins?

Last updated on June 8th, 2023 at 03:11 pm

You don’t have to be involved with cryptocurrency for a long period of time to understand that the price of most cryptocurrency assets are extremely volatile. This volatility makes maintaining value in regular transactions difficult at best. Stablecoins provide an alternative to these extreme price fluctuations.

Stablecoins are a cryptocurrency whose price is pegged to a fiat currency or commodity. Stablecoins can be broken into two categories, collateralized stablecoins and algorithmic stablecoins. Collateralized stablecoins can be broken into fiat backed, crypto backed and commodity backed stablecoins.

Stablecoins offer the convenience and security of crypto with the stability of fiat currency. While the idea and use of stablecoins currently fills a need in the cryptocurrency space, there are distinct advantages and disadvantages of each type.

Moreover, there is a discussion to be had regarding the ability of stablecoins to help with crypto adoption, as well as the long term need for stablecoins as the cryptocurrency market matures.

What Are Stablecoins?

Let’s begin our dive into the world of stablecoins with this perplexing fact… stablecoins are not coins, they are tokens.

This is because stablecoins run on another coin’s blockchain. If you haven’t already discovered what a token is, you should familiarize yourself with cryptocurrency tokens.

As we get back to the definition of a stablecoin, in the most simple terms, a stablecoin is a cryptocurrency asset that is designed to have its price pegged to the value of another asset. This makes stablecoins an excellent medium of exchange and in times of extreme volatility, a good store of value.

Think of a stablecoin as the blockchain version of a fiat currency or the blockchain version of a commodity.

Most stablecoins are pegged in price to the U.S. Dollar (USD). This makes sense because, as of this writing, USD is currently the world reserve currency.

Other stablecoins are pegged to different fiat currencies, such as the EURO. This helps to facilitate the exchange of these national currencies on cryptocurrency exchanges to allow for trading and purchasing of crypto assets.

How a stablecoin maintains its value peg indicates what category of stablecoin it is, as well as if it is a centralized or decentralized asset.

Moreover, there have been concerns that stablecoins are not decentralized. This concern is not just related to the stablecoins blockchain itself, but also the fact that the majority of stablecoins are controlled by a small group.

Top 5 USD Stablecoins By Marketcap

Collateralized Stablecoins

Much like the name suggests, collateralized stablecoins are ones that are backed by another asset or commodity.

This type of stablecoin can further be broken down into stablecoins that are collateralized on chain or off chain.

Off Chain Fiat Collateralized Stablecoins

This group represents the most widely used type of stablecoins in the cryptocurrency space. These stablecoins are generally backed by USD or the fiat currency they are pegged to.

So, in theory, there should be 1 USD held in reserve for every 1 stablecoin.

This requires users of this type of stablecoin to trust that the stablecoin issuer actually has these funds, and they are held in a secure location. Furthermore, users must trust that when this type of stablecoin is redeemed for USD, that the stablecoin is burned, thus removing it from the supply.

Many stablecoin issuers will have a private third party audit their reserves to ensure compliance. This helps to instill confidence to retail and institutional investors as well as making an attempt to keep regulatory bodies at bay.

As you can imagine, this requires a centralized entity to facilitate these actions. Due to this high degree of centralization, the possibility of control and manipulation of this type of stablecoin is extremely high. Furthermore, the level of privacy with this type of stablecoin is greatly reduced.

The largest stablecoin in this group is Tether (USDT).

Tether has been mired with controversy regarding the liquidity of its backed assets, in this case USD, for many years. They have thus far been able to provide proof of more than 70% liquidity, though this was not all in actual USD reserves.

Off Chain Commodity Collateralized Stablecoins

Much like their fiat backed counterparts, this type of stablecoin maintains its peg by being backed by a physical asset such as gold.

These stablecoins were designed to provide investors greater access to these commodities. Think of these like ETFs (Exchange Traded Funds). An ETF allows you to trade the asset, without actually owning the asset.

In this group of stablecoins, the most popular commodity to use for collateralization is gold. This makes sense as gold has been a medium of exchange and a store of value for thousands of years.

So, in theory, there should be an ounce of gold held in reserve for every 1 stablecoin.

Again, just like its fiat backed counterpart, these commodity based stablecoins require a centralized entity who must be trusted to hold the tangible asset securely. They must also be trusted to ensure the proper redemption or exchange of the stablecoin.

These stablecoins provide holders proof-of-reserves by being audited by a third party.

The largest commodity backed stablecoin by marketcap is Paxos Gold (PAXG).

One of the primary advantages to this type of stablecoin is that they are more resistant to inflation like the commodities they represent.

On Chain Collateralized Stablecoins

This group of stablecoins is backed by a basket of other cryptocurrency assets. Due to the inherently volatile price action of cryptocurrency, these types of stablecoins are over collateralized.

Over collateralization means that the reserves of these stablecoins are a much higher amount than the peg they hold. Usually, an on chain stablecoin will hold at least 150% of the assets in reserve to help offset the price fluctuations.

Algorithmic Stablecoins

This group of stablecoins is not backed by a tangible asset. These stablecoins maintain their peg using code or smart contracts. This makes them decentralized by nature and helps to better maintain privacy for those transacting with them.

Algorithmic stablecoins utilize smart contracts to manipulate the circulating supply. The stablecoins in this group utilize one of the following algorithms to maintain their price peg, Rebase, Seigniorage or Fractional algorithmic.

The smart contracts that govern these stablecoins all work similarly. However, thus far they have met with limited success.

Rebase Algorithmic Stablecoins

Currently this algorithmic process is the most widely utilized.

This type of stablecoin maintains its price peg by manipulating the circulating supply of the token via smart contract. In essence, using supply and demand to dictate how the smart contract operates.

So, in theory, when the stablecoin price rises above $1, new tokens are minted to increase the circulating supply, thus devaluing the token and returning the price to its peg. When the price lowers below $1, tokens are burned to decrease the supply, thus raising the value of the token and returning the price to its peg.

While this seems like a good means of maintaining a price peg, the crypto space has already seen this type of stablecoin fail.

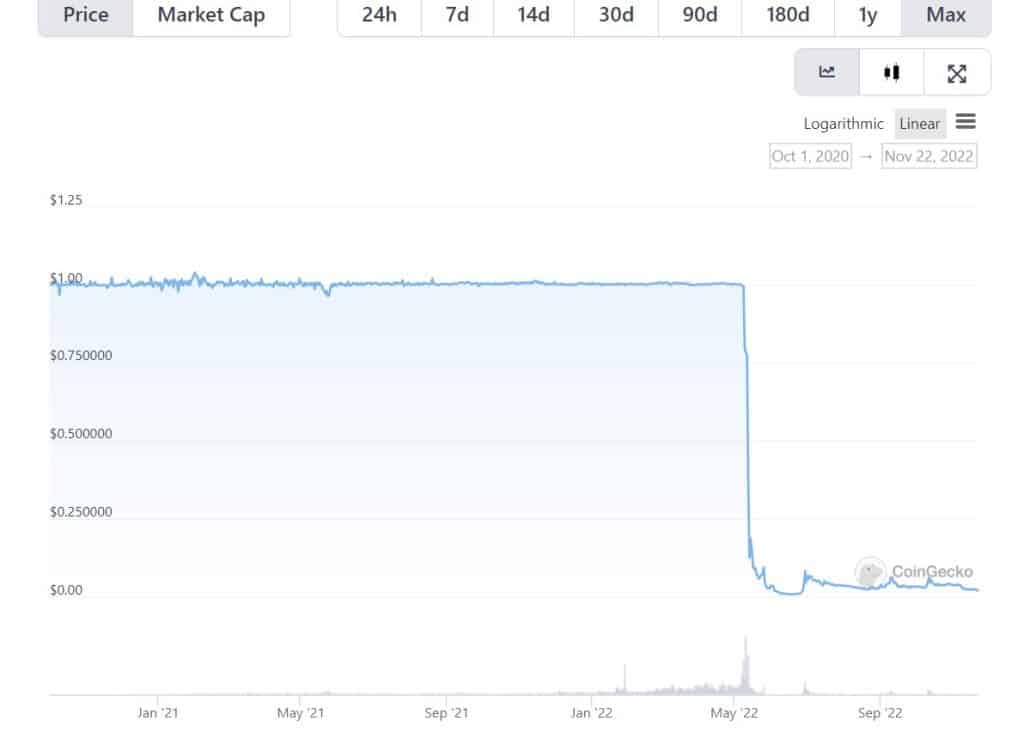

In May of 2022, Terra USD (UST) became depegged from its $1 price point was unable to recover. This happened during extreme volatility, which caused a bank run on the stablecoin, ultimately causing a cascading downward price spiral.

Seigniorage Algorithmic Stablecoins

In a nutshell, this type of stablecoin utilizes one or more coins to maintain its price peg.

This stablecoin maintains its price with a supply manipulating algorithm like the rebase model, in combination with free market behaviors from the associated coin. This is meant to trading of non-stable crypto assets.

For those not familiar with the term, a free market is one that is free of government influence and regulation.

So, in theory, the free market helps to maintain the peg of the stablecoin.

Fractional Algorithmic Stablecoins

This type of stablecoin takes a page out of the fractional reserve banking playbook.

In fractional reserve banking, banks are only required to keep a portion of the customer assets they hold on hand at any given time.

This is why in times of crisis, when customers flood banks to get their funds out, the banks close or restrict the amount of money withdrawn because they do not actually have those funds on hand.

This has happened in India, the world’s third largest economy, on multiple occasions.

This type of stablecoin is essentially a combination of the previous two. The stablecoin is partially backed by assets, and the peg is maintained by using smart contracts which manipulate the token supply.

So, in theory, this type of stablecoin enjoys the partial backing of another asset, while utilizing supply and demand pressures to maintain the peg.

Frax Finance (FRAX) is one such stablecoin.

Stablecoins currently fill a void in the crypto space by providing stable crypto assets to trade with. This leaves some to ponder the question of stablecoins being a catalyst for cryptocurrency adoption.

Stablecoins and Crypto Adoption

Given that stablecoins are designed to be less volatile than their crypto cousins, it has been postulated for years that these stablecoins can fit into the mainstream economy.

Afterall, getting businesses and retailers to accept stablecoins as payments seems to make sense.

Given their quick settlement, businesses can rest assured that ‘a dollar is a dollar,’ and that dollar is in their account immediately, not 24-48 hours later, like how commercial banks operate.

Not to mention that the fees associated with stablecoins are certainly much less than those being charged by these traditional banks, especially when it comes to the processing of credit card transactions.

For most businesses in the United States, commercial banks charge the business 1.5% to 3.5% on average for the ability to accept credit cards as a form of payment.

Given that 80% of consumers prefer using credit cards over cash, this can be a huge drain on a business’ bottom line.

In fact, many small businesses pass these fees back to the consumer. Maybe you have seen these surcharges or convenience fees on some of your recent bills. Businesses are actually given advice on how to do this while still complying with a state’s consumer protection laws.

With all of this, you would think that using stablecoins would be embraced by many businesses. Unfortunately, as of this writing, this is not the case.

Many business owners see cryptocurrency, including stablecoins, as too volatile and risky.

Not to mention, it is easier to stay with what you know… in this case, the traditional banking system.

However, there are signs that stablecoins have made some inroads.

In 2019, the Securities and Exchange Commission (SEC) said it would begin running stablecoin nodes.

Then in 2021, banks in the United States received the go ahead from the Office of The Comptroller of Currency to start accepting stablecoins as a form of payment settlements.

While these moves have not made stablecoins a part of the settlement structure for small businesses in the U.S. yet, they have prompted lawmakers to begin debating regulations for these assets.

This rush to regulation has been fueled by negative happenings in the crypto space. These include the Terra USD stablecoin collapse, the FTX Exchange collapse.

However, the government has other motives for regulating stablecoins. This is because the government is working toward the issuance of a Central Bank Digital Currency (CBDC).

The Future of Stablecoins

As I mentioned earlier in this article, stablecoins are currently filling a much needed role within the cryptocurrency space. Being a medium of exchange from fiat to crypto assets, as well as being a store of value during times of extreme volatility is certainly something the crypto market needs.

However, the question of the continued need for stablecoins as the cryptocurrency space grows and matures is up for debate.

Generally speaking, a large, very liquid market does not experience the wild price fluctuations that are currently experienced almost daily in crypto.

So, as the crypto market increases in size, it stands to reason that the huge price fluctuations we currently see would settle, and digital asset prices would become more stable. Thus, reducing or completely eliminating the need for stablecoins.

This becomes an even more lively debate if the use of stablecoins as a settlement medium does not materialize.

Combine that possibility with the realization that governments across the globe are developing and deploying their own CBDCs. The likelihood that governments are going to leave potential competition alive and well is very low.

However, even if stablecoins are not the future of money, I would argue that Bitcoin or some other, possibly many other, cryptocurrencies would be. Even if this means the development of a parallel economy, outside of the influence of governments.

These are some of the ideas I discuss as I lay out the reasons I believe cryptocurrency will one day replace the U.S. dollar. Furthermore, I make the case for cryptocurrency being better than banks and ultimately better for the world.

However, before you consider digesting those articles, you should have a more complete understanding of cryptocurrency, particularly what is is and how it works.

Disclaimer

The information provided here is for INFORMATIONAL & EDUCATIONAL PURPOSES ONLY!

View our complete disclaimer on our Disclaimer Page